If you’ve ever wondered why your credit score seems to bounce around from month to month even when you pay your bills on time, the answer is often hiding in a simple number: your credit utilization ratio.How Credit Utilization Affects Your Credit Score

This single factor is the second most important component of your credit score, accounting for 30% of the FICO calculation . Only your payment history matters more. Yet it’s also one of the most misunderstood and easiest to optimize once you know how it works.

In this guide, we’ll break down exactly what credit utilization is, how it impacts your score, what the “ideal” ratio really is, and practical strategies to keep it working for you—not against you.

What Is Credit Utilization?

Credit utilization is simply the amount of credit you’re using compared to your total available credit. It’s expressed as a percentage .

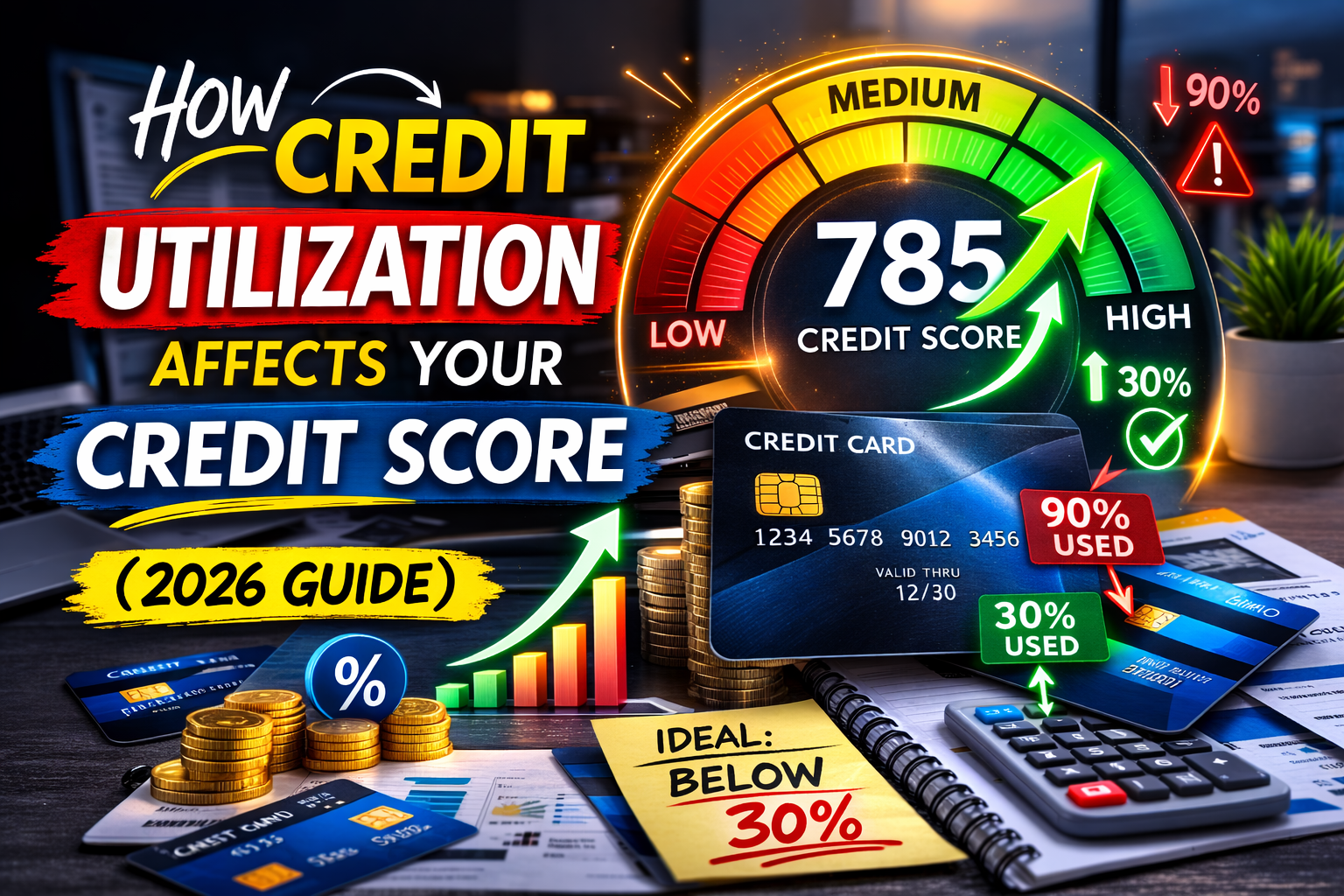

Think of it this way: If you have a credit card with a $10,000 limit and you currently have a $3,000 balance, your utilization on that card is 30%.

The same concept applies across all your revolving credit accounts. Lenders and credit scoring models look at both:

- Per-card utilization: The balance on each individual card relative to its limit

- Overall utilization: The sum of all your balances divided by the sum of all your credit limits

This distinction matters because you could have excellent overall utilization but a single maxed-out card that raises red flags .

Why Utilization Matters So Much

Credit scoring models use utilization to answer a fundamental question: Can you manage credit responsibly without overextending yourself?

Someone who uses a small portion of their available credit appears less risky. They have access to funds but don’t desperately need them. Someone consistently near their limits looks stretched thin—more likely to miss payments or default if an unexpected expense arises .

This isn’t just theoretical. Studies consistently show that utilization is one of the strongest predictors of future credit risk. People with high utilization are statistically more likely to fall behind on payments, so the scoring models penalize that behavior .

The “Ideal” Utilization: What the Numbers Really Say

You’ve probably heard the rule of thumb: keep your credit utilization below 30%. This is good advice, but it’s not the whole story.

The 30% Rule

The 30% threshold is widely cited because it’s a meaningful cutoff in the scoring algorithms. Utilization above 30% starts to negatively impact your score, and the higher you go, the more damage it does .

But here’s the nuance: 30% isn’t a magic number where everything is fine below it and terrible above it. Utilization is a continuous variable—lower is almost always better, down to a certain point .

The 10% Advantage

If you really want to maximize your score, research suggests keeping utilization below 10% is even better . This is the range associated with the highest scores. People with exceptional credit (scores above 800) typically have very low utilization ratios.

The 0% Exception

This is where it gets counterintuitive. While low utilization is good, 0% utilization can actually hurt your score slightly compared to a very low non-zero percentage .

Why? Because 0% utilization means you’re not actively using your credit. The scoring models have less information about how you manage revolving debt. A small balance that you pay off each month demonstrates responsible credit management more effectively than no balance at all .

This doesn’t mean you should carry debt and pay interest—never do that. But if your statement closes with a small balance that you then pay in full by the due date, you’re in the optimal zone. You show responsible usage without paying a dime in interest .

How Utilization Is Calculated

Understanding the timing is crucial because it explains why your score can change even when you haven’t made a major purchase.

Credit card issuers typically report your balance to the credit bureaus once a month, usually on your statement closing date . This is the date your billing cycle ends and your statement is generated.

Here’s the key: The balance reported is whatever was on your card on that specific day—not your average balance for the month, and not necessarily the balance when you pay your bill.

This means you could:

- Use your card heavily during the month

- Pay the entire balance before the due date

- Never pay interest

- Still have a high utilization reported if you paid after the statement closing date

The balance on your statement is what gets reported to the bureaus. If that number is high, your utilization looks high—even if you pay in full every month and never carry debt .

How Much Your Score Can Change

The impact of utilization on your score can be dramatic. Depending on your starting point, optimizing your utilization could boost your score by 20, 50, or even 100 points .

Someone with a maxed-out card at 90% utilization who pays it down to 10% could see a significant jump in just a month or two. Conversely, someone who pays off a large balance and closes the account might see a temporary drop because their available credit decreased .

The exact impact depends on the rest of your credit profile, but utilization is one of the fastest-moving factors in credit scoring. A change in reported balances can affect your score within weeks .

Strategies to Optimize Your Utilization

1. Pay Down Balances Strategically

The most direct way to lower utilization is to reduce your balances. If you have multiple cards, focus on the ones closest to their limits first, because high per-card utilization hurts more than overall utilization alone .

2. Pay Before the Statement Closing Date

This is the single most effective tactic for people who use credit cards regularly but pay in full. If you know your statement closing date (check your online account or call your issuer), make a payment a few days before to bring your balance down to a low single-digit percentage .

Your reported balance will be low, your utilization will look great, and you’ll still pay nothing in interest because you’re paying the remaining balance by the due date.

3. Request a Credit Limit Increase

If you can’t pay down your balance quickly, increasing your available credit is the other side of the equation. A higher limit on an existing card instantly lowers your utilization .

For example, a $2,000 balance on a $5,000 limit is 40% utilization. If the issuer increases your limit to $8,000, that same $2,000 balance becomes 25% utilization—without you spending a dime.

Most issuers can grant increases with a “soft inquiry” that doesn’t affect your score, based on your history with them . Call and ask, or check your online account for pre-approved offers.

4. Spread Balances Across Cards

If you have a card that’s near its limit, consider moving some of that balance to another card with a lower rate or spreading spending across multiple cards to keep individual utilization low .

This doesn’t reduce your total debt, but it improves per-card utilization, which matters to the scoring models. Just be mindful of balance transfer fees if you’re moving balances between issuers.

5. Don’t Close Old Cards

Closing a credit card reduces your total available credit, which can increase your overall utilization ratio . Even if you don’t use an old card, keeping it open helps your utilization (and your average age of accounts).

If there’s an annual fee you don’t want to pay, consider asking the issuer to downgrade to a no-fee version rather than closing the account entirely.

6. Add Multiple Payments Per Month

If you use credit cards heavily for everyday spending and rewards, you can make multiple payments throughout the month to keep your balance low at all times .

This is especially useful if you’re approaching a major application (like a mortgage) and want your score maximized. Pay whenever you get paid, and your reported balance will never get too high.

7. Become an Authorized User

If someone with a long history of low utilization adds you as an authorized user on their card, that account’s positive payment history and low utilization can benefit your score .

This only works if the primary cardholder manages the account responsibly. If they miss payments or max out the card, it will hurt your score instead of helping.

Common Misconceptions

“I need to carry a balance to build credit.”

This is one of the most persistent myths in personal finance. You do not need to carry a balance or pay interest to build credit. Paying your balance in full each month builds credit just fine, and it’s better for your wallet .

“Utilization is a long-term factor.”

Utilization has no memory in current scoring models. Unlike late payments, which stay on your report for seven years, utilization resets each month based on the latest reported balances . This means you can improve your score relatively quickly by paying down debt.

“Only overall utilization matters.”

Both overall and per-card utilization matter. Having one maxed-out card can hurt your score even if your total utilization looks fine . The scoring models want to see responsible management across all your accounts.

“0% utilization is optimal.”

As mentioned earlier, a very low non-zero utilization (say, 1-5%) actually scores slightly better than 0% because it shows you’re actively using credit responsibly . Don’t carry debt to achieve this, but don’t stress if a small balance reports before you pay it off.

Utilization in Special Situations

Between Jobs or Tight on Cash

If you’re going through a tough financial period and your balances are high, focus on the basics: make at least minimum payments on time, and don’t open new credit you can’t manage. Your score will recover as your balances come down.

Approaching a Major Loan Application

If you’re planning to apply for a mortgage, auto loan, or rental in the next few months, optimizing your utilization should be a top priority. Start paying down balances and make extra payments before statement closing dates to get your reported utilization as low as possible .

Lenders pull your credit at application, and lower utilization can mean better interest rates—potentially saving you thousands over the life of a loan.

After Paying Off a Large Balance

If you pay off a large credit card balance, celebrate—that’s a huge win. But don’t close the card immediately if it has no annual fee. Keeping it open maintains your available credit and helps your utilization long-term.

The Bottom Line

Credit utilization is one of the most powerful levers you have to control your credit score. Unlike payment history, which requires years of consistent behavior, utilization can be optimized in a matter of weeks with the right strategies.

The key takeaways:

- Keep overall utilization below 30%, and ideally below 10%, for the best scores

- A small non-zero balance (paid in full each month) is better than 0%

- Pay attention to statement closing dates—they determine what gets reported

- Request credit limit increases to improve your ratio without paying down debt

- Don’t close old cards that help your available credit

- Utilization resets monthly, so improvements happen quickly

Your credit score is a tool, not a report card. Understanding how utilization works gives you control over that tool. Use it wisely, and it will serve you well when you need it most.

1 thought on “How Credit Utilization Affects Your Credit Score (2026 Complete Guide)”